A couple weeks ago, at BIA/Kelsey ENGAGE, I made the comment that the local on-demand industry has achieved “peak-Uber,” when the company seems inevitable and unbeatable but will be hard-pressed to continue to raise capital at the break-neck pace it has over the past three years. The news that Uber smashed the one-round record for capital raised earlier this week with a $3.5 billion investment from Saudi Arabia’s Public Investment Fund only reinforces my conviction that Uber’s run as a darling of disruption-lovers is ending.

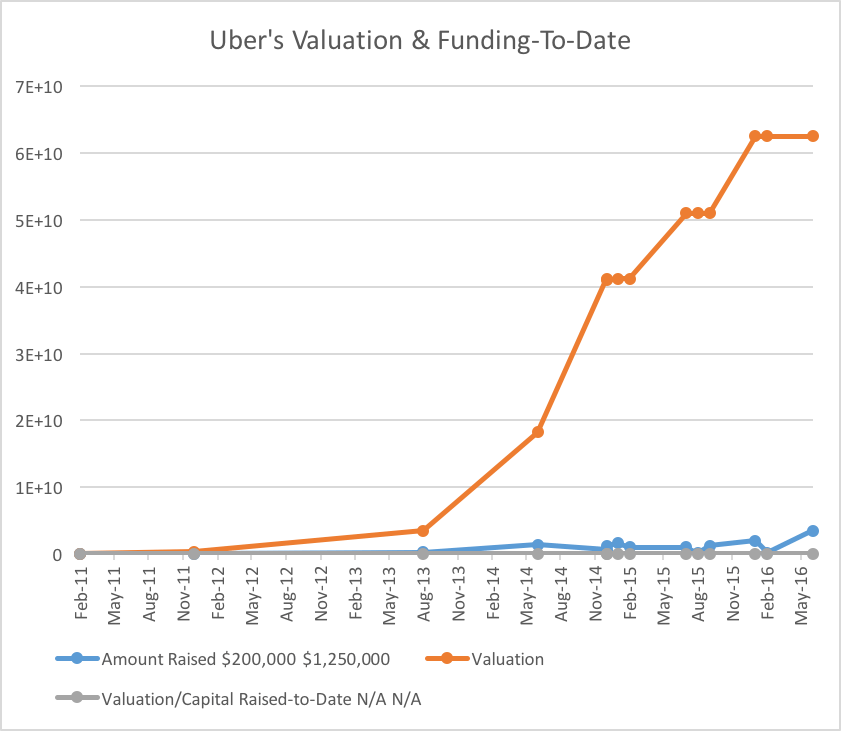

Uber will not be able to sustain its growth without an immediate increase in profit. Why? Because the cost of capital at Uber is rising precipitously. With the $3.5 billion Saudi-contributed round, which brings the total capital raised by Uber to $14.11 Billion, according to Crunchbase, Uber effectively jumped the financial shark when it paid slightly more for the cash than it did at its A-Round in 2011.

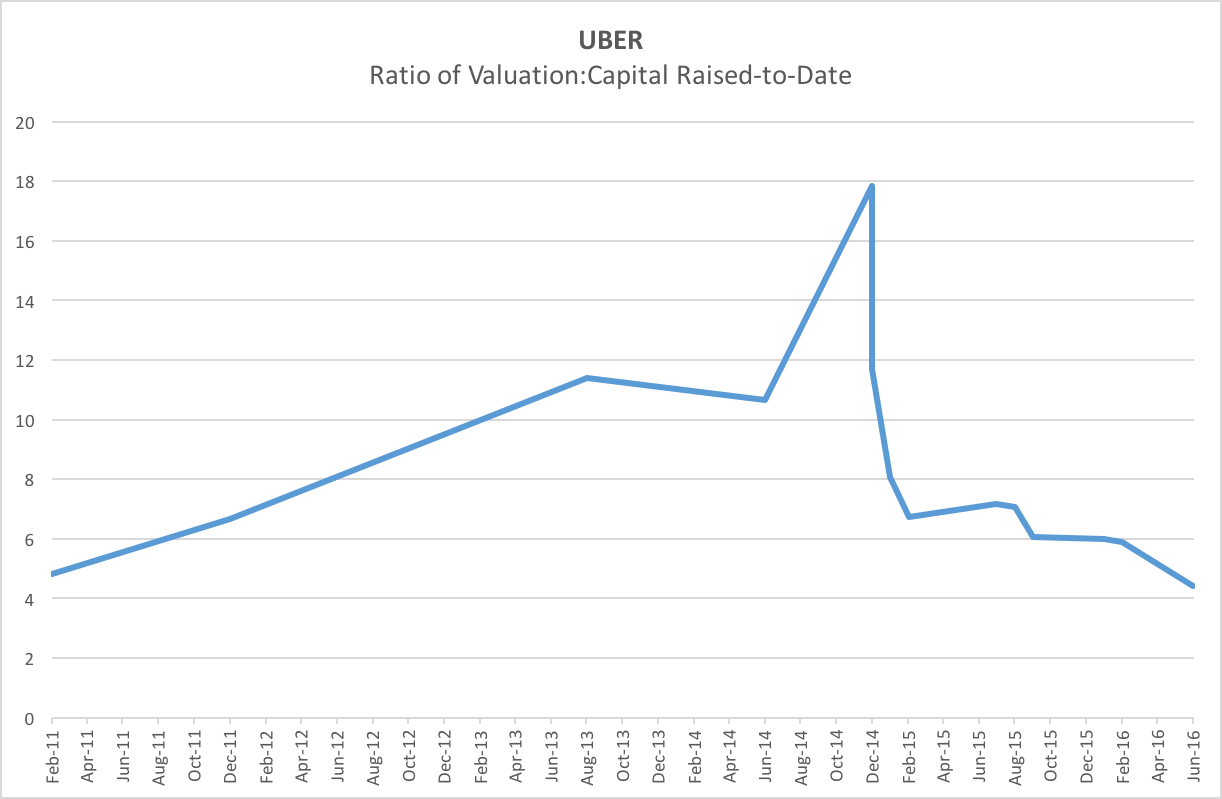

In 2011, after two angel rounds totaling $1.25 million, Uber vaulted into the big time with an $11-million round that valued the company at $60 million. At that time, the ratio of valuation to capital raised was 4.82 times post-money value. This week’s $3.5 billion raise came at a Valuation:Capital-Raised ratio of 4.43.

Uber’s ability to command a significant premium in all previous rounds, which reached a peak of 17.85 times capital raised to date in the fall of 2014, is exhausted. Only a permanent move to profitable operations will change the value of the company.

Uber’s ability to command a significant premium in all previous rounds, which reached a peak of 17.85 times capital raised to date in the fall of 2014, is exhausted. Only a permanent move to profitable operations will change the value of the company.

A glance at the valuation ratio chart suggests that Fall 2014 was “peak Uber” in terms of the ability to raise capital, but the company’s achievements and PR/political efforts remain a potent force in business conversation. And, obviously, it was able to raise $3.5 billion more this week. However the company paid 25 percent more in shares this time, based on estimates extrapolated from its stated post-money valuation, than it did just four months ago, when it closed a round of $200 million.

Based on its current performance, there is simply nowhere left for Uber equity to go but down. The IPO window may have closed for the company.

What does post peak Uber look like? The company is fighting for market share globally, partnering with potential fleet providers that are positioned to offer mobility through any marketplace, including their own, should they choose to launch their own Uber competitors.

Market share is a famously ephemeral advantage, it is not an asset. Yet Uber’s market share is the primary driver of its valuation, it is everything the company invests to acquire. Consequently, the shape and financial size of Uber’s business is increasingly speculative and risky, so investors demand more for their money each round.

Market share is a famously ephemeral advantage, it is not an asset. Yet Uber’s market share is the primary driver of its valuation, it is everything the company invests to acquire. Consequently, the shape and financial size of Uber’s business is increasingly speculative and risky, so investors demand more for their money each round.

Uber has also committed to buy $10 billion worth of Mercedes autonomous vehicles, adding to its future capital needs. It’s not clear that autonomous vehicles will arrive in volumes necessary to eliminate Uber’s drivers from the ride equation, which Uber CEO Travis Kalanick has said will make the company profitable. Moreover, the cost of managing a fleet of autonomous cars could cost as much or more than paying contractors to provide and maintain their own vehicles.

There is no clear path to profitability for Uber, given its global footprint and the amount and variety of competition emerging in every market. From its traditional foes, Lyft and Didi Chuxing, to driver-led cooperatives and alternative transportation offerings, especially in the emerging economies where a rickshaw ride can be faster than a traffic-bound car ride, Uber is fighting for its life on every front.

At today’s 4.43x premium, Uber’s stock is already priced below the long-expected IPO investors have hoped will yield a huge payday. Early investors, particularly in the explosive rounds between $60M and $41B in value, can still make a significant return, but any future investors will be looking at a one-to-three-times return or less. Since a return is not guaranteed, those investors will not be as eager to participate and Uber’s value will go down, making it harder to sustain its strategy globally and forcing decisions that could revalue Uber significantly below its current price.

So finely tuned financially, Uber cannot sustain a down round. Uber won’t necessarily fail or disappear into the bowels of an acquiring automaker. Yet is it time to recognize the company doesn’t have a lock on the future of transportation. It may be the icebreaker that goes too far in a season and ends up locked in the ice while others sail on.